Sick Of Struggling And Getting Denied

Every Time You Need Money?

Book a quick Funding & Strategy Call to see EXACTLY why lenders keep saying no—and how to start positioning yourself toward $10K–$50K in personal and business funding with real banks and credit unions REGARDLESS of your past credit.

This Funding & Strategy Call is designed to help you:

Stop guessing and see exactly why your applications keep failing.

Discover which 2–3 moves can make the biggest difference fastest.

Start moving toward $10K–$50K in funding in a legal, realistic way—especially if you are self‑employed or rebuilding.

Real People. Real Approvals. See What the Community is Saying.

Do You Need Money To Start Or Grow Your Business, But Don't Know Where To Get It?

You're not alone. The world of business funding is tricky. It's full of red tape, and making a mistake can cost you a lot.

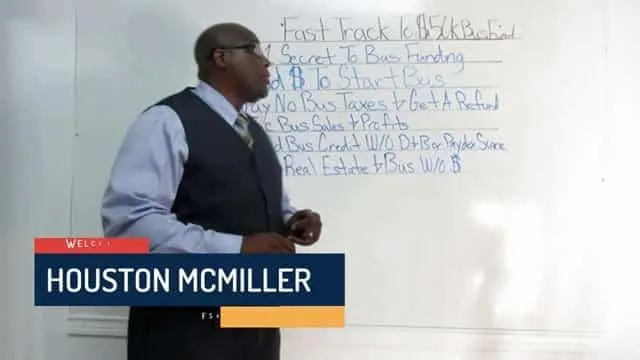

Houston McMiller has the answer. His Fast Track to $50,000 in Business Funding is a free video series. He shares top secrets that only 10% of small businesses know.

You'll learn how to get funds fast, avoid mistakes, and cut through the red tape.

HoustonMcmiler.net

Business Credit America, Inc.

269 S Beverly Dr #725

Beverly Hills,CA 90212

+1 888 883 3013

Disclaimer & Advertiser Disclosure:

HoustonMcmiller.net is an independent, advertising-supported comparison service. The offers that appear on this site are from companies from which we may receive compensation. This compensation may impact how and where products appear on this site, including the order in which they appear. This site does not include all companies or all available financial offers.

Editorial Note: The opinions, reviews, and recommendations expressed here are the author’s alone and have not been reviewed, approved, or otherwise endorsed by any financial institution or card issuer. We strive for accuracy, but information is provided "as-is" and offers are subject to change without notice. We are not licensed financial advisors, attorneys, or accountants; the content provided is for informational purposes only and should not be taken as legal or financial advice. Please consult with a professional regarding your specific situation.

2026 © Business Credit America, Inc. All Rights Reserved.

2022 All Rights Reserved.